VA Home Loan Guaranty

Buyer’s Guide

Version: April 2022gf

1

Table of Contents

Overview ....................................................................................................................................................... 3

Outline of the VA Homebuying Process ........................................................................................................ 5

Eligibility ........................................................................................................................................................ 6

Before Borrowing .......................................................................................................................................... 9

Beginning the VA Home Loan process .................................................................................................. 9

Some helpful tips: ............................................................................................................................... 10

General Mortgage Costs ..................................................................................................................... 11

Buying a Home with a VA-Guaranteed Loan .............................................................................................. 14

Additional VA Loan Options ........................................................................................................................ 15

Energy Efficient Mortgage (EEM) ........................................................................................................ 15

Alteration and Repair loan .................................................................................................................. 16

Construction Loan ............................................................................................................................... 17

Farm Residence Loan .......................................................................................................................... 19

Loan Assumption ................................................................................................................................. 20

Required Loan Documents .......................................................................................................................... 22

Lender-Required Documents .............................................................................................................. 22

VA-Required Documents ..................................................................................................................... 22

The VA ‘Escape Clause’ ............................................................................................................................... 23

VA Appraisal ................................................................................................................................................ 23

What if my appraisal is below the purchase price? ................................................................................ 24

Home Inspections ....................................................................................................................................... 25

Negotiable items ..................................................................................................................................... 27

At Closing: Buying Your Home .................................................................................................................... 28

Post-Purchase: Mortgage Servicing ............................................................................................................ 29

Escrow Accounts ................................................................................................................................. 29

Appendix A: Military Service Requirements ............................................................................................... 31

Veterans and Active Duty Service members ....................................................................................... 31

National Guard and Reserve members ............................................................................................... 31

Exceptions to minimum service requirements ................................................................................... 32

Other Than Honorable, Bad Conduct, or Dishonorable discharges .................................................... 32

Appendix B: Certificate of Eligibility (COE) .................................................................................................. 33

How to apply for a COE ........................................................................................................................... 33

Proof of Service Requirements ............................................................................................................... 33

Character of Service (COS) Requirements .............................................................................................. 34

Notes on Reserve and National Guard COS requirements ................................................................. 35

Upgrading discharge status ................................................................................................................. 35

Appendix C: Funding Fee Tables ................................................................................................................. 36

Appendix D: Reusing the VA Loan ............................................................................................................... 37

Re-using your VA Loan benefit (Restoring Entitlement) ..................................................................... 37

Buying Another Home (Remaining Entitlement) ................................................................................ 37

Appendix E: Eligible Spouses ....................................................................................................................... 40

How to apply for Dependency and Indemnity Compensation (DIC): ................................................. 41

Surviving Spouses applying for VA Home Loan eligibility: .................................................................. 41

Appendix F: Native American Direct Loan (NADL) Program ....................................................................... 43

NADL Eligibility .................................................................................................................................... 43

Appendix G: How to Avoid Foreclosure ...................................................................................................... 45

2

If You Cannot Make Payments on the Due Date?............................................................................... 45

What If I Experience Financial Troubles? ............................................................................................ 46

Beware of the "Dotted Line" ............................................................................................................... 46

Appendix H: FAQs and Common Issues ...................................................................................................... 48

Appendix I: Terms and Definitions .............................................................................................................. 50

3

Overview

Created by the original G.I. Bill (Servicemen’s Readjustment Act of 1944), the VA-Guaranteed Home Loan

program has helped generations of Veterans, Servicemembers, and their families enjoy the dream of

homeownership and the opportunity to retain their homes in times of temporary financial hardship.

Should you have any questions about the VA Home Loan benefit or issues with your current home loan,

feel free to contact us at: 1-877-827-3702.

What is the VA Home Loan ‘Guaranty’?

The VA home loan guaranty is an agreement that VA will reimburse a lender (such as banks, credit

unions, mortgage companies, etc.) in the event of loss due to foreclosure. This guaranty takes the place

of your down payment.

Who is eligible for a VA Home Loan?

Active-duty servicemembers and Veterans with discharges other than dishonorable, National Guard and

Reserve service members and Veterans with an honorable discharge, certain eligible spouses, and other

uniformed service personnel may be eligible for VA home loan guaranty benefits. The full listing is

available online at: https://www.va.gov/housing-assistance/home-loans/eligibility/.

Is there a fee to use the VA Home Loan Guaranty?

Yes, but the funding fee can be waived (see list below). To keep the program viable, Congress instituted

a program funding fee, which is a percentage of the total loan amount. This user fee varies based

whether the loan is a first-time or subsequent (second, third, etc.) use of the benefit. The funding fee

may be paid in cash or included in the loan at closing.

*The funding fee can also be paid by the seller, lender, or any other party on your behalf. (See

Chapter 8 of the Lenders Handbook)

The following individuals do not pay the VA funding fee:

• Veterans receiving VA compensation for a service-connected disability.

• Veterans entitled to receive VA compensation for a service-connected disability, but receive

retirement pay or active service pay.

• Unremarried surviving spouses of Veterans who died in active service or from a service-

connected disability.

• Service member with a proposed or memorandum rating from VA, prior to loan closing, as

eligible to receive compensation as a result of a pre-discharge claim.

• Service member on active duty who provides, on or before the date of loan closing, evidence of

having been awarded the Purple Heart.

Is there a limit to the size of a VA-backed mortgage?

There are no loan limits if one has full home loan benefit or full entitlement. If you are a first-time

homebuyer or have sold your previous VA-backed home and paid your loan in full, you can enjoy VA-

backing on a home loan regardless of home price and without the need for a down payment.

1

Of

course, you must be able to afford the home and the property must appraise for at least the purchase

price, otherwise you may have to make a small down payment.

1

Blue Water Navy Vietnam Veterans Act of 2019, https://www.congress.gov/bill/116th-congress/house-

bill/299/text

4

Note: For loans made prior to 2020 that exceeded the Freddie Mac conforming loan limit, lenders

required borrowers to pay a down payment for the loan amount above the county loan limit.

What if I want to buy a home while I still have another VA Home Loan?

While you can buy a home for any loan amount, you must either sell your previous home or understand

VA rules on subsequent purchases and remaining entitlement. Those who purchase a subsequent home

without selling their previous VA-guaranteed home will continue to follow their county conforming loan

limit for the VA loan guaranty. This may mean a down payment on any amount above the loan limit.

Note: You must be able to afford all your VA loans at the same time and the subsequent home must

become your residence. (See Appendix D: Reusing the VA Loan below or this blog)

Why choose VA?

The VA Home Loan is often the best home loan product for Veterans. Some benefits include:

• No down payment as long as the sales price is at or below the home’s appraised value (the

value set for the home after an expert review of the property) See VA Appraisal section below

• No loan limit with full entitlement if you can afford the loan, VA will back loans in all areas of

the country, regardless of home price.

• Competitive terms and interest rates from private banks, mortgage lenders, or credit unions

• No need for private mortgage insurance (PMI) or mortgage insurance premiums (MIP)

o PMI is a type of insurance that protects the lender if the borrower ends up not being

able to pay the mortgage. It’s usually required on conventional loans if the down

payment is less than 20% of the total mortgage amount.

o MIP is what the Federal Housing Administration (FHA) requires borrowers to pay to self-

insure an FHA loan against future loss.

o Not having to pay PMI could save a borrower on their monthly mortgage payment

• Fewer closing costs, which may be paid by the seller, lender, or any other party

• No penalty fee for paying off the loan early

• Access to VA loan staff who can answer questions by mail or phone (1-877-827-3702). (Contact

information is online at: https://www.benefits.va.gov/homeloans/contact_rlc_info.asp)

See more frequently asked questions in Appendix H: FAQs and Common Issues.

5

Outline of the VA Homebuying Process

Buying a home can seem intimidating to first-time homebuyers. The intent of this guide is to help

alleviate some of that stress by giving you the information you’ll need to make the decisions right for

you.

This guide is organized to explain the general VA homebuying process in a linear fashion. You can start

with VA – from starting the home shopping through what do if you need to avoid foreclosure in the

future.

What you need to know when buying a home with the VA home loan:

• Verify your VA Home Loan eligibility (or if you meet the criteria for surviving spouse eligibility)

• Learn about the basics of home-buying before you shop around

• Apply for your VA home loan Certificate of Eligibility (or apply through your lender)

• Know the additional loan options for VA home loans

• Gather the required documents to provide to your lender

• Learn about the VA appraisal and ‘VA Escape Clause’

• Some things to know after you close on your loan

Additional sections of this document include:

• Military service requirements, exemptions and other than honorable discharges

• Funding Fees

• Reusing the VA loan

• Who are eligible surviving spouses

• How to avoid foreclosure

• Some frequently asked questions

6

Eligibility

Based on your service to the country, you may be eligible for the VA Home Loan benefit. VA is the only

organization that can determine eligibility for a VA direct or VA-backed home loan benefit based on your

length of service or service commitment, duty status, and character of service. Details for determining

eligibility (including calculating credible years of service) can be found in Chapter 7 of the M26-1

Guaranteed Loan Processing Manual.

Lenders’ Borrowing Requirements:

You must meet your lender’s minimum or standards of credit, income, and any other requirements to

approve a loan. VA does NOT require a minimum credit score, but most lenders will use a credit score to

help determine your interest rate and to lower risk. Typically, lenders may want borrowers to have a

minimum credit score.

Because different lenders have different requirements, feel free to shop around for a lender that meets

your financial and homebuying needs.

VA’s Borrowing Requirements:

VA does not determine how much you can borrow. However, unlike other loans, VA requires you to

have enough income remaining after paying your mortgage and other financial obligations. This helps

ensure you can afford homeownership and lessen the risk of defaulting on your loan.

Also, you must:

1) live in the home being bought with the loan, and

2) meet ONE of the following:

Active-Duty Servicemember: Currently on active duty and have served at least 90 continuous days.

Note: Active duty includes Active Guard Reserve (AGR) members activated under Title 10 U.S.C.

Veteran: Veterans separated from active duty between August 2, 1990 and the present (Gulf War era)

must have served:

• 24 continuous months, or

• A full period (at least 90 days) for which you were called or ordered to active duty, or

• At least 90 days if discharged for a hardship, a reduction in force, or for convenience of the

government, or

• Less than 90 days (if discharged for a service-connected disability)

Note: This includes Reserve and National Guard members called to active duty for at least 90 days.

Active duty does not include active duty for training.

NATIONAL GUARD on Active-duty:

• At least 90 days of non-training active-duty service (shown on DD214 for the activation or

any other documents to support the activation), OR

• At least 90 days of active service including at least 30 consecutive days (shown as 32 USC

sections 316, 502, 503, 504 or 505 activation on your DD214, annual point statements,

DD220 with accompanying orders, or any other documents to support the activation)

RESERVE on Active-duty:

• At least 90 days of non-training active-duty service (shown on DD214 or any other

documents to support the activation)

7

A full listing of length of service requirements for other eras is located here.

Reserve / National Guard Service member: If not otherwise eligible (e.g., with prior active duty or

Title 10 or Title 32 service listed under the ‘Veteran’ section above), this includes those currently serving

in the Selected Reserve or National Guard (member of an active unit, attending required weekend drills,

and two-week active duty for training). You must complete a total of six credible years and ONE of the

following:

• Continue to serve in the Selected Reserve.

• Serve as Active Guard Reserve (AGR).

• Placed on the retired list.

• Transferred to the Standby Reserve or an element of the Ready Reserve other than the Selected

Reserve after service characterized as honorable service.

Note: AGR Service members (on Title 32 U.S.C. orders) and Individual Mobilization Augmentee

(IMA) Service members must meet the 6-year requirement. Periods of Inactive Ready Reserve (IRR)

service are NOT creditable toward the 6-year requirement.

Reserve / National Guard Veteran: If not otherwise eligible (see ‘Veteran’ section above), you must

have completed a total of six credible years in the Selected Reserve or National Guard (member of an

active unit, attended required weekend drills and two-week active duty for training) and ONE of the

following:

• Discharged with an honorable discharge, or

• Placed on the retired list, or

• Were transferred to the Standby Reserve or an element of the Ready Reserve other than the

Selected Reserve after service characterized as honorable service.

Note: Periods of Inactive Ready Reserve (IRR) service are NOT creditable toward the 6-year

requirement Individuals who completed less than six years may be eligible if discharged for a

service-connected disability. For discharge status that is not honorable, see the Other Than

Honorable, Bad Conduct, or Dishonorable discharges under Appendix A below.

Eligible Spouses: The spouse of a Veteran can also apply for home loan eligibility if they 1) are eligible

for, or in receipt of, a qualifying Dependency and Indemnity Compensation (DIC) benefit award, and 2)

under ONE of the following conditions:

• Unremarried surviving spouse of a Veteran who died while in service (active, reserve, or national

guard) or from a service-connected disability, or

• Unremarried surviving spouse of certain totally disabled (100% rated) Veteran whose disability

may not have been the cause of death, or

• Surviving spouse who remarries on or after December 16, 2003 after attaining age 57, or

• Spouse of a living Service member missing in action (MIA) or a prisoner of war (POW) for more

than 90 days, for as long as the Service member is in that status (this is one-time use only)

2

Note: More information is available below in Appendix E: Eligible Spouses

2

See paragraph 3 of 38 U.S.C §3701(b)

8

Other eligible borrowers:

• A U.S. citizen who served in the Armed Forces of a government allied with the United States in

World War II

• Served as a member in certain organizations, such as:

o Cadet at the United States Military, Air Force, or Coast Guard Academy

o Commissioned Officers of the Public Health Service

o Officer of the National Oceanic & Atmospheric Administration (NOAA)

o Midshipman at the United States Naval Academy

o Merchant seaman during World War II

• Details for other eligible borrowers can be found in Chapter 7 of the M26-1 Guaranteed Loan

Processing Manual

9

Before Borrowing

Before buying a home, you should consider the costs and benefits of homeownership. While renting a

home can offer flexibility and limited responsibility for maintenance, rent can change over time, the

owner can sell the property, and you may or may not receive your security deposit when you move.

Homeownership, over the long-term can offer benefits such as relatively stable monthly mortgage

payments and a way to build wealth for you and your family.

VA highly recommends that you determine your priorities before buying a home, such as what you are

willing to spend each month on a mortgage and what other expenses (vehicle, childcare, etc.) you will

have to consider. Only you can determine what meets your housing and financial needs.

Note: The Consumer Financial Protection Bureau (CFPB) offers tools and resources to help you

find the right home loan for you at: https://www.consumerfinance.gov/owning-a-home/.

When you are ready to buy a home or refinance your loan, VA will be there to serve you

throughout the life of the loan.

Beginning the VA Home Loan process

Below are the general steps for starting the home buying process.

1. Apply for your VA home loan Certificate of Eligibility (COE) – The COE verifies to

your lender that you qualify for the VA home loan benefit. If you have used your loan benefit in

the past, a current COE may be helpful to know how much remaining entitlement you have or to

ensure your entitlement was restored for previous VA-backed loans that were paid in full.

2. Look at your current finances – Review your credit profile, income, expenses, and

monthly budget to make sure you’re ready to buy a home. Decide how much you want to spend

on a mortgage—and be sure to include closing costs in the overall price. Get more advice from

the Consumer Financial Protection Bureau.

3. Choose a lender – You can go through a private bank, mortgage company, or credit union to

get your loan. Lenders offer different loan interest rates and fees, so shop around for the loan

that best meets your needs.

4. Choose a real estate agent – Meet with several real estate agents and then select one to

represent you in the homebuying process. You can take your lender’s pre-approval letter to your

real estate agent and begin shopping. Read all agreements—and make sure you understand any

charges, fees, and commissions—before signing with an agent. Remember they work for you

and should put your interests first.

5. Shop for a home – Look at houses in your price range until you find one that works for you.

10

Some helpful tips:

• Know your lender’s credit requirements – VA does NOT require a minimum credit

score, but most lenders will use a credit score to help determine your interest rate. Typically,

lenders may want borrowers to have a minimum credit score of 620, unless there is a large

down payment.

• Know what is in your credit history – Consumer Financial Protection Bureau (CFPB)

recommends that borrowers get a free copy of their credit report from the three nationwide

credit reporting companies. This also offers an opportunity to correct errors and strengthen

your scores:

o Visit AnnualCreditReport.com, OR use the automated phone system at 1-877-322-8228

Note: Anyone can receive one free credit report from each company, every 12 months

• Shop around for a lender – Lenders offer competitive interest rates, fees, and closing

costs on VA-backed purchase loans. You can start by looking around for a network of people and

information you trust to help you through the process. You can start gathering facts about your

finances, so you’ll have them ready at your fingertips.

o Ask multiple lenders for a Loan Estimate and review the helpful guide on comparing

loan offers at: https://www.consumerfinance.gov/owning-a-home/process/compare/

Note: Multiple credit checks from mortgage lenders within a 45-day window are

recorded on your credit report as a single inquiry.

3

o Explore interest rates with CFPB’s Interest Rate Explorer:

https://www.consumerfinance.gov/owning-a-home/explore-rates/

• Loan term – VA loans can be issued for 30 years or 15 years. Shorter-term loans typically have

a lower interest rate and lower total cost; however, they also have higher monthly payments.

See more comparisons at: https://www.consumerfinance.gov/owning-a-home/loan-options/.

o Note: For VA home loans, you can pay off (amortize) your loan with NO penalty or early

payoff fee.

• Fixed or ARM – VA loans can be a fixed-rate or adjustable rate mortgage (ARM)

o Fixed rate mortgage – (the most common VA loan option) This mortgage option has a

set principal and interest payment throughout the life of the loan, no matter how rates

change nationally. You may see slight increases in your monthly mortgage payment each

year due to changes in local property taxes and insurance.

o ARM – This is where your loan interest rate is adjusted periodically, based on an index.

These loans may have a low introductory rate, but the rate can grow over time and so

will your monthly mortgage payment.

o More information on loan types is available at:

https://www.consumerfinance.gov/owning-a-home/loan-options/

3

CFPB, What exactly happens when a mortgage lender checks my credit? https://www.consumerfinance.gov/ask-

cfpb/what-exactly-happens-when-a-mortgage-lender-checks-my-credit-en-2005/

11

• Energy and improvements – VA offers two loan options that can be utilized in

conjunction with a VA purchase or refinance loan. These loans must be closed along with your

VA loan. (See Energy Efficiency Improvement and Alteration and Repair loan sections below)

• Purchasing a condo – VA maintains a list of approved condos. If the condo is not on the list,

the project must be submitted to VA for review to ensure that it complies with VA requirements.

(See Chapter 10 of the Lenders Handbook) For additional questions, you can contact VA at 1-

877-827-3702.

• Selling your current home to buy another – Generally, you can hold multiple home

loans if you can afford all the loans. If your plan to purchase a new home is contingent on selling

your current home, your lender can disregard the payments on the outstanding mortgage(s) and

any consumer obligations that you intend to clear. Just be sure to speak with your lender on any

required documentation.

• Adverse items on your credit – In circumstances not involving bankruptcy, satisfactory

credit is generally considered to be re-established after you have made satisfactory payments

for 12 months after the date the last derogatory credit item was satisfied.

o In cases of bankruptcies – see Chapter 4 of the Lenders Handbook, Topic 7: Credit

History – Required Documentation and Analysis.

General Mortgage Costs

Buying a home requires both one-time and recurring costs. VA policy allows sellers, lenders, or any other

party to pay loan fees and charges on behalf of the borrower. (See Chapter 8 of the Lenders Handbook)

Although some additional costs are unique to certain localities, the closing costs generally include VA

appraisal, credit report, survey, title evidence, recording fees, a 1 percent loan origination fee, and

discount points. The closing costs and origination charge may not be included in the loan, except in VA

refinancing loans.

VA requires you to have enough cash assets to cover:

• Closing costs, pre-paid costs, or discount points which are the borrower’s responsibility and are

not financed into the loan

• The difference between the sales price and the loan amount, if the sales price exceeds the

reasonable value established by VA (i.e., negative equity)

Note: VA does not require you to have additional cash to cover a certain number of mortgage

payments, unplanned expenses or other contingencies on the residence, or refinance of a residence.

However, you may want to consider saving money for unforeseen circumstances or large purchases,

such as replacing appliances, replacing a roof, or re-painting walls.

Can I include any fees into the loan? The VA funding fee, if appliable, can be included in the

purchase loan. No other fees and charges or discount points can be included in the loan amount for

purchase or construction loans. Only refinancing loans may include other allowable fees and charges

and discount points in the loan amount.

Below are some expenses for you to consider when you determine your financial plans for buying and

maintaining a home.

12

One-Time Expenses

When purchasing a home there are will be many fees and options for you to consider. Some are

required by VA or the lender, while others are optional, but may serve you as you make the investment

in a home. This list in not all-inclusive.

• VA Funding Fee – This is the user fee to utilize the VA home loan. Some borrowers may be

exempt from paying the fee. (see Appendix B: VA Funding Fee Tables for percentage or

exemption)

• Appraisal – (Mandatory) The appraisal is required for purchase and cash-out refinance loans.

A VA-approved appraiser will determine a reasonable value of the home. VA can then determine

how much, if not all, of your loan to guarantee. The notice of value (NOV) generated from the

appraisal provides comprehensive information on the home and may help you know if the home

meets basic property requirements. (See Chapter 12 of the Lenders Handbook for more on

minimum property requirements) The NOV can also help you choose whether to continue with

the purchase or negotiate price or other conditions of the sale. (See Escape Clause section

below)

• Closing Costs – (Mandatory) The fees paid at closing include (but not limited to) taxes,

transfer fees, origination fees, and other customary costs. The seller, lender, or any other party

can pay for fees and charges on your behalf. You can negotiate with the seller on splitting these

costs, if any concessions do not exceed 4% of the sale. (see Chapter 8 of the Lenders Handbook)

• Down payment – (Optional) If you choose to make one, this one-time cost can help lower

both your monthly payment and overall outstanding loan amount.

o Note: If your down payment is at least 5-percent, you can pay a lower VA funding fee, if

you are not already exempt. (see Appendix C: VA Funding Fee Tables)

• Discount Points – (Optional) While most lenders offer VA Home Loan borrowers

competitive rates, borrowers can also opt to pay for an even lower interest rate by paying for

discount points. The seller, lender, or any other party can pay for discount points (or other fees

and charges) on your behalf. (see Chapter 8 of the Lenders Handbook)

• Earnest Money Deposit – (Optional) This is a cash deposit used to hold a home you are

bidding on. It shows that you are serious about purchasing that home.

• Home Inspection – (Optional) VA highly recommends that you get a third-party to conduct

a thorough inspection of the home. This is in addition to the appraisal. Your appraisal does not

take the place of an inspection. You don’t want to be surprised by something that will cost you

later to repair or replace. (see Home Inspections section below)

• Lender’s Title Insurance –– (Optional) Most lenders require title insurance to protect

them against legal claims against the home.

• Owner’s Title Insurance – (Optional) While owner’s title insurance is optional, it is highly

recommended to purchase this one-time premium insurance. This can protect you if someone

has a claim against the home before you purchased it, such as home repairs that weren’t paid

off when the seller sold the home.

13

Recurring Expenses

Beyond the purchase of your new home, you must consider the full cost of home ownership. This is not

an all-inclusive list, but

• Mortgage payment – This monthly expense includes payment towards the loan principal,

interest, homeowner’s insurance, and your estimated property taxes. (see CFPB article for

further explanation)

• Homeowner’s insurance – This is required for all mortgages. VA highly recommends that

you shop around to find the coverage that can cover your home and personal property in the

home, such as clothing and high-value items.

• Utilities and Maintenance – This may include water, electricity, and gas. Maintenance

costs can include general servicing or replacement of heating and cooling systems, water

heaters, laundry machines, refrigerators, and ovens.

• Homeowner’s/Condominium association fees – If required, these fees go towards

upkeep of property and other services provided by the association, such groundskeeping,

swimming pools, and security.

14

Buying a Home with a VA-Guaranteed Loan

Buying a home is a process. It requires a combination of filling out forms, verifying ability to pay, and

meeting the interests of both buyer and seller. Getting a VA-backed home loan is only one piece of the

puzzle. Here are some general steps in the home buying process:

4

Lenders offer competitive interest rates on VA-guaranteed loans. This can help borrowers buy a home—

especially if they don’t want to make a down payment. You may be able to get a VA-guaranteed

purchase loan if you meet all the requirements listed below:

1. Qualify for a VA-guaranteed home loan Certificate of Eligibility (COE), and

2. Meet VA—and your lender’s—standards for credit, income, and any other requirements, and

3. Will live in the home you’re buying with the loan

If eligible for a VA-guaranteed purchase loan, you can use the loan to:

• Buy a single-family home, townhouse, or multi-family up to 4 units

• Buy a condo in a VA-approved project

• Buy a home and improve it

• Buy a manufactured home and lot

• Build a new home

• Make changes or add new features to make the home more energy efficient (see EEM section

above)

You can also:

• Re-use a VA loan benefit if selling or refinancing a home bought with a VA-guaranteed home

loan,

• Assume a VA-backed home loan (which means that instead of opening a new mortgage loan, the

buyer takes over the seller’s loan)

Note on purchasing a condo: VA maintains a list of approved condos. If the condo is not on the

list, the project must be submitted to VA for review to ensure that it complies with VA requirements.

(See Chapter 10 of the Lenders Handbook) For additional questions, contact VA at 1-877-827-3702.

For more information, please visit the VA Home Loan program home page at:

https://www.benefits.va.gov/HomeLoans/index.asp.

4

Source: https://www.va.gov/housing-assistance/home-loans/loan-types/purchase-loan/

15

Additional VA Loan Options

When purchasing or refinancing a home, you have some additional loan options that can used in

conjunction with your VA home loan. You can opt to make energy efficiency or other improvements

when you purchase the home. However, these loan options must be closed at the same time as you

close your VA home loan. So be sure negotiate with your lender prior to closing your VA home loan

when you find the option that is best for your situation. (see Chapter 7 of the Lenders Handbook)

Energy Efficient Mortgage (EEM)

EEMs are loans that cover of the cost of making energy efficiency improvements to a home. VA allows

up to $6,000 worth of improvements to be included in your loan. While this will slightly increase your

monthly payment, the cost is normally offset by a reduction in utility costs over time.

You may wish to contact a qualified person or firm for a home energy audit to identify recommended

energy efficiency improvements. In some areas, the utility company may perform this service.

Energy efficiency improvements may include (but not limited to):

• Solar heating and cooling systems

• Caulking and weather stripping

• Furnace efficiency modifications

• Clock thermostats

• New or additional insulation

• Storm windows/doors

• Heat pumps

• Other energy related improvements may also be considered

Note: An EEM is not a separate VA home loan product. An EEM can only be used in conjunction with a

VA purchase loan, or an interest rate reduction refinance loan (IRRRL) secured by the dwelling. It must

also be closed at the same time as the VA loan is closed.

If you are interested in making energy improvements, be sure to find a lender willing and able to do this

type of loan. Some lenders may not have experience with EEMs, but they can review Chapter 7 of the

Lenders Handbook or contact the nearest VA Regional Loan Center.

It is important that you work with your lender early in the loan process to determine the cost of

improvements, monthly mortgage increase, and any funding fee increase.

Generally, efficiency improvements must be complete either before or within six months after loan

closing. Your lender will set up an escrow to pay for any improvements after loan closing.

Note: You are not required to make improvements. Even after loan closing, you can contact your

lender to cancel the EEM if you decide that improvements do not meet your personal, financial, or

housing needs.

16

Alteration and Repair loan

VA understands that the aging housing stock in the United States has contributed to an increased

demand for alteration and repair loans. You can use the VA home loan to purchase or (cash-out)

refinance homes that need alteration and/or repair.

5

VA can guarantee a loan for alteration and repair:

• Made in conjunction with a purchase loan on the property, OR

• Cash-out refinance of a residence you already own and occupy as a home

Note: For purchase loans, VA will guarantee the lesser of the acquisition cost OR as-completed value

determined by the VA appraiser. For refinance loans, you can use the as-completed value in the

transaction.

VA allows improvements to be included in the value and completed after closing of the loan. Loan

proceeds are paid out to the builder and/or contractor during the alteration/repair period. The lender

must obtain written approval from you before each disbursement or draw payment to the builder

and/or contractor.

You can alter a home to your preference, but the alterations and repairs must be those ordinarily found

on similar property of comparable value in the community. Also, they must bring the home up to the

VA’s minimum property requirements. (See Chapter 12 of the Lenders Handbook for more on minimum

property requirements)

Some common alterations and repairs include (but not limited to): roof, foundation, floors,

plumbing, electrical, and HVAC system.

You may want to seek advice of an inspector or structural engineer for recommended upgrades. Also,

VA highly recommends that you first consider the full cost of renovating a home, including anticipated

and unanticipated costs (which can grow as new issues are found) and may include:

• Permit, inspection, title costs

• Labor costs

• Structural work

• Finance costs

• Removal of debris

• Changes in scope of work

Note: Not all lenders are able or willing to close alteration and repair loans. And not many lenders

have experience with these loan types. Be sure to shop around for a lender that will meet your

personal, financial, and housing needs.

To determine the acquisition costs for a purchase, add the following: Contract sales price, total cost of

alterations and repairs, contingency reserve (if any up to 15 percent of the repair cost), inspection fees,

title update fees, and permits.

Do I need to put in any money?

A contingency reserve is not required however, your lender may consider a contingency reserve if

the project warrants it. The maximum contingency reserve is 15 percent of the alteration and/or

repair cost.

5

The terms alteration, repair, renovation, and improvement are interchangeable

17

• For purchases, any unused contingency reserve funds are applied to the principal balance,

unless it was paid in cash at closing. If you paid in cash, it can be returned to you.

• For refinances, any unused contingency reserve funds may be returned to you or applied to

the principal balance at your discretion.

Can I choose my builder or contractor?

Yes, you are free to choose your builder or contractor. However, they must be register with VA to

obtain a VA builder identification number. (See Chapter 10 of the Lenders Handbook) Your lender

may have additional requirements, such as ensuring the builder or contractor is licensed, bonded,

and insured according to state and local requirements. A list may be found at

https://lgy.va.gov/lgyhub/.

Instructions to become a registered builder with VA are at

https://www.benefits.va.gov/HOMELOANS/appraiser_cv_builder_info.asp.

What if I change my mind on upgrades during construction?

You are permitted to pay for change orders and upgrades out of pocket. Any change order or

upgrade made after the appraisal cannot be mortgaged into the new loan unless the appraisal is

updated. Change orders must be approved, in advance, by the appraiser, to ensure there is no loss

in value. If an appraisal is to be updated, your lender will be responsible for contacting the appraiser

with the documented change order(s). You can pay an additional appraisal charge if change orders

are requested. This additional appraisal charge may come out of available contingency reserve

funds.

Construction Loan

The VA home loan can be used to construct a new residence. You can use the construction loan to build

a home on property that you already own or want to buy as part of the loan.

Note: Construction loans include loans do not include newly developed properties where a builder is

using their own funds for construction. You can still use the VA loan to purchase the property from

the builder.

You must find a participating VA lender which offers options for construction loans. The interest rate

varies from lender to lender, so VA strongly encourages you to shop around to multiple lenders to

ensure you get the best rate and terms available for your mortgage needs. Once you decide on a

participating lender, you can complete the building and lending process, to include closing the loan and

paying all applicable fees.

(See Chapter 7 of the Lenders Handbook for more on construction home loans)

Note: Not all lenders are willing or able to offer construction loans. These types of loans and

projects inherently have uncertain elements that require more careful examination compared to

traditional purchase loans. Be sure to find a lender with specialized experience to originate, process,

underwrite (you, project, and builder), close, service and administer such loans.

Typically, construction timelines are established as part of the contract. Your lender is responsible for all

aspects of project management and may set specific limitations. VA will not issue a Certificate of

Guaranty to the lender until completion of the project.

18

Construction loans are closed prior to the start of construction with proceeds disbursed to cover the

cost to build, cost of the land, or balance owed on the land, with the remaining balance in escrow,

sometimes referred to as a Loan in Process (LIP) account, or a Draw account.

The escrowed monies are paid out to the builder during construction. Your lender must obtain your

written approval before each disbursement, or draw payment, is provided to the builder.

You don’t not have to make payments on your home loan until after construction is complete. The initial

payment on the principal may be postponed up to 1 year. For example, if you have a 30-year mortgage

and construction takes 6 months to complete, then you must repay your loan in 29 years and 6 months.

You can work with your lender as to whether you have a balloon payment at the end of your loan or set

up slightly larger payments to avoid the balloon payment.

Also, during construction, the builder is responsible for interest payments and all fees normally paid by

builders with interim construction loans, such as inspection fee, title updates, title update fees, hazard

insurance, and property taxes.

Two types construction to permanent loans:

• One-time close (or single close) construction loan – This loan is used to close both the

construction loan and permanent financing at the same time. The permanent financing is

established prior to construction, and the final terms are modified to the permanent terms at

the conclusion of construction.

General Process:

1) Your lender verifies your eligibility and entitlement.

2) Your lender orders an appraisal “based on Plans and Specs,” if the appraisal can be

completed before the completion of the foundation.

(Note: For projects farther along than the completion of the foundation, the appraisal

must wait until construction is complete)

3) VA issues the Notice of Value (NOV) to you and your lender.

4) Your loan closes.

5) Unless exempt, you must pay the funding fee within 15 days

6) Builder completes construction.

7) Final inspection or CO signifies the end of the project.

8) Your lender modifies your loan.

• Two-time close construction loan – This loan generally involves an initial loan closing prior to

the start of construction, and a second closing where permanent financing is used to take out,

or replace the initial loan

General Process:

1) Your lender verifies your eligibility and entitlement.

2) Your lender orders an appraisal “based on Plans and Specs,” if the appraisal can be

completed before the completion of the foundation.

(Note: For projects farther along than the completion of the foundation, the appraisal

must wait until construction is complete)

3) VA issues the Notice of Value (NOV) to you and your lender.

4) Your lender closes the initial loan with non-VA financing.

5) Builder completes construction.

19

6) Qualify the borrower(s) again.

7) Order the appraisal, if appropriate.

8) Issue the NOV, if appropriate.

9) Your loan closes.

10) Unless exempt, you must pay the funding fee within 15 days

Can my builder finance construction?

Yes, the builder can finance the construction from his or her own resources.

When do I have to pay the VA funding fee?

Unless you are exempt from paying it, the VA funding fee is due at loan closing prior to the start of

construction. Your lender must submit that fee payment to VA within 15 days of loan closing. Payment

is not tied to the start or completion of construction.

How is my interest rate set?

Your lender may offer a “ceiling-floor” where the interest rate “floats” during construction. The

agreement must provide that at lock-in, the permanent interest rate will not exceed a specific maximum

interest rate while allowing you to lock-in at a lower rate based on market fluctuations. Interest rates

vary from lender to lender. The rates available to the Service member or Veteran borrower will vary

based on specific lender criteria for approving the loan and what the bank or non-bank lender offers,

and VA strongly encourages all borrowers seeking to acquire a loan and purchase a home to shop

around multiple lenders to ensure that they obtain the best mortgage terms available to them. Note:

You must qualify for the mortgage at the maximum rate.

Farm Residence Loan

You can use your VA home loan benefit to purchase, construct, repair, alter, or improve a farm

residence that you intend to occupy. You can also use the loan to construct a farm residence on land

you already own. (See Chapter 7 of the Lenders Handbook)

The VA-guaranteed loan cannot cover:

• Non-residential value of farmland in excess of the home site, OR

• Barn, silo, or other outbuildings necessary for farm operations, OR

• Farm equipment or livestock

Note: When constructing a farm residence on land you own, you may use a portion of the loan to

pay off liens on the land only if the reasonable value of the land is at least equal to the amount of

the lien(s).

You can start a business on the farm you purchase, but keep in mind that the VA loan benefit exists to

help you buy a home, not start a business. The VA loan can be used to purchase the residential portion

of the farmland. However, you would need to secure a separate loan to purchase the non-residential

portion of the land and any building or equipment associated with farming operations.

20

If you plan to use farming operations income to support your loan payments, your lender will have to

determine your ability and experience as a farm operator. The general procedures and analysis provided

under “Self-Employment Income” is in Chapter 4 of the Lenders Handbook.

For new farmers, your lender will need the following:

• Your proposed plan for farm operations, including the number of acres for each crop, number of

livestock, etc., to estimate your potential income and expenses.

• A statement that you own or will purchase the farm equipment required to operate the farm. If

you will incur additional debt when purchasing this equipment, your statement should contain

full details as to repayment terms, etc.

• An estimate of farm income and expenses by a local farm appraiser designated by VA or another

qualified person, or the estimate used by a lender offering you an operating line of credit. The

estimate should be based on your proposed plan of operation, ability and experience, and the

nature and condition of the farm, including livestock and livestock products. The expense

estimate must detail labor, seed, fertilizer, taxes and insurance, repairs, machinery, fuel, etc.

• A copy of a commitment from a lender for an operating line of credit or evidence of the

resources to be used to cover operating expenses.

For experienced farmers continuing the same farm operation:

• If you finance operations from an operating line of credit, you will need to provide records of

advances from, payments to, and carryover balances on the operating line of credit for at least

the last 3 years.

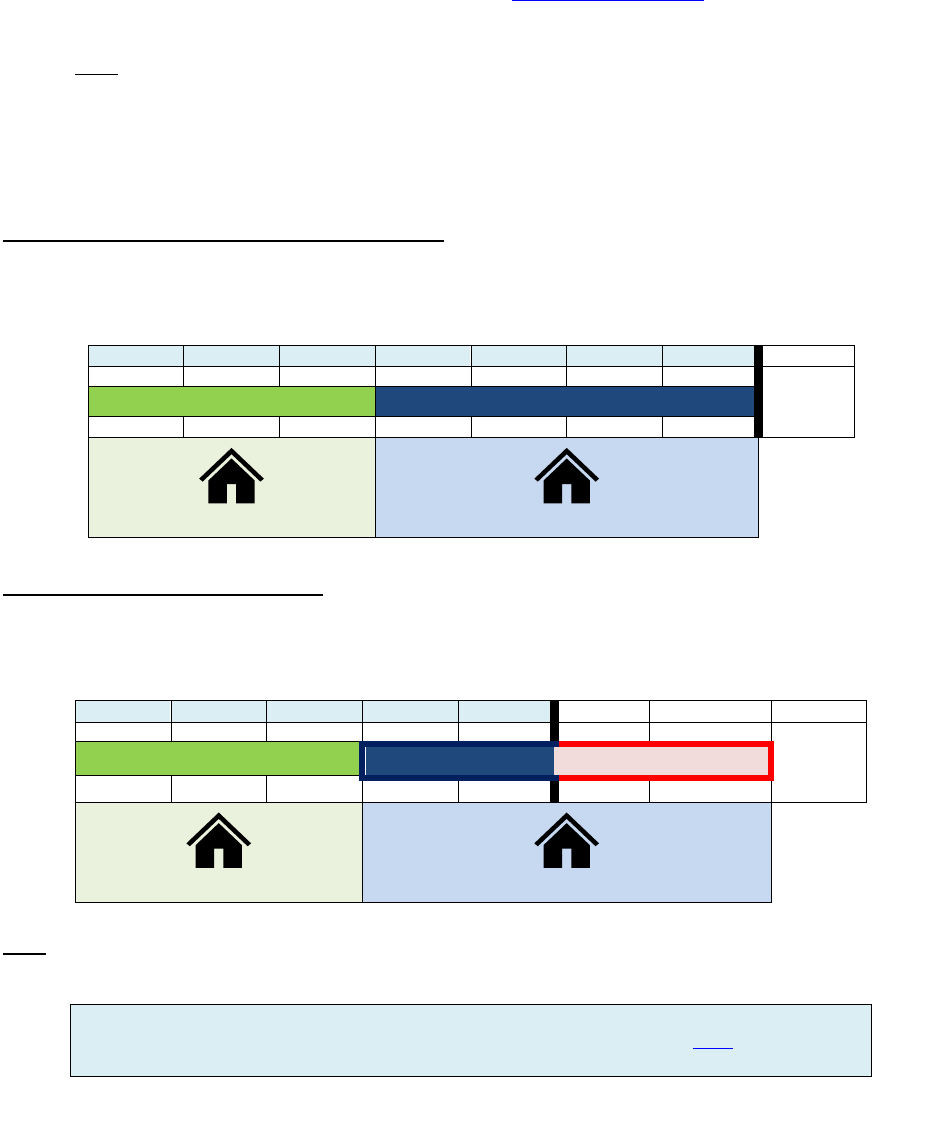

Loan Assumption

One feature of the VA home loan is that is assumable. This means that anyone can assume, or take over

payment, on a VA home loan, if they qualify. It is a unique feature that gives you the option to purchase

a home with a previously set interest rate or, in a time of need, avoid foreclosure.

There could be a situation where you are unable pay back your loan or maybe you are simply unable to

sell a home in your area. In any case, this feature of the VA home loan is meant to serve your needs.

Why would this be a benefit to you?

• When interest rates rise, assuming a low interest rate VA home loan could make the home more

desirable to a purchaser

• The funding fee (unless exempt) is only 0.5%

• A Veteran can substitute their own VA home loan entitlement to assume your loan, thereby

allowing VA to restore your entitlement, assuming the other Veteran has enough entitlement to

cover your loan

• Anyone, even a non-Veteran, can assume your loan, but in such case your entitlement remains

with the loan

• Any equity in the home remains with the loan, however you can negotiate with the buyer on

cashing out some or all the equity as part of the sale

VA home loan assumption requires servicer approval, and in some instances VA approval. Be sure to

work with your servicer to obtain approval for assumption. They will usually perform an income and

credit check to be sure the assumer is a good risk and is not likely to default on the loan.

21

Note: You should be highly selective about who assumes your VA home loan. If there is a default on

an assumed loan, it will count against the original veteran’s entitlement and may affect your chance

of securing another VA loan.

If another eligible borrower substitutes their VA entitlement, the following forms are required:

• Either a COE or fully completed VA Form 26-1880 (Request for a Certificate of Eligibility) for the

assumer. The assumer must have enough entitlement to substitute for that of the original

Veteran.

• A signed VA Form 26-8106 (Statement of Veteran Assuming GI Loan). The assumer must certify

that the property securing the loan will be occupied as their home.

Note: If VA uses your entitlement to pay a claim on a defaulted loan, even if that loan has been assumed

by someone else, you can’t use that entitlement amount on a new loan. You must repay the claim

amount to VA before your entitlement is restored. However, either you or the person that assumed

your loan can repay it.

22

Required Loan Documents

Just as anyone with a mortgage will tell you, there are a lot of forms to fill out when you’re applying for

a mortgage. The loan process begins with you filling out forms and providing copies of financial

documents to help your lender to determine the size and terms of your loan.

Lender-Required Documents

Most lenders will require documents to estimate the amount they can lend you, the interest rate, and

any other requirements for loan approval. These documents include, but are not limited to:

• Your Certificate of Eligibility (COE) or VA Form 26-1880 (Request for a Certificate of Eligibility)

• Uniform Residential Loan Application (URLA) – a Freddie Mac Form 65 or Fannie Mae Form 1003

is required for all home loans

• Credit report

6

• Proof of income (2-year minimum of employment):

o Pay stubs, including LES for military employment

o W-2 forms or income tax returns

o Bank statements

o Proof of other income (including but not limited to investments, rental properties, etc.):

• Documentation of outstanding debts:

o Including student loan, car loan, child support, alimony, and other debts

o Your lender may use this information to determine if your other debts may affect your

ability to make monthly mortgage payments

• (if applicable) Homeowner’s or Condominium association forms

• (if applicable) Gift letter for gift funds provided by someone not involved with the sale

o (Rules for gift funds are in Chapter 4 of the Lenders Handbook)

VA-Required Documents

When you request a VA home loan certificate of eligibility (COE), VA will verify your eligibility for a VA-

guaranteed loan and whether you are exempt from paying the VA funding fee due to VA rating for a

service-connected disability. Your lender will likely provide you with these forms, but you may download

and fill out these forms electronically on your own. You will need to fill out and provide your lender with

the following documents with your loan application:

• Your COE or a VA Form 26-1880

• VA service-connected disability award letter if not noted on COE (to verify funding fee

exemption)

• Condo form (*if applying for a condo)

Note: Although your lender may provide paper copies of these forms, we have provided the links to

the most current version of the forms so that you can electronically fill out the information and

submit clear copies with your loan application.

If your lender does not know which forms are currently required, you can refer them to the VA Lenders

Handbook for the most current VA requirements.

6

Note: VA does NOT require a minimum credit score. However, most lenders will use your score to help

determine your interest rate. Feel free to shop around for a lender that meets your financial and homebuying

needs.

23

The VA ‘Escape Clause’

When you find the home that is right for you, your real estate agent can help you develop an offer,

create the sales contract, and assist you with the negotiation process. Remember to include in your

sales contract, a contingency (called an ‘escape clause’) which allows you to not incur any penalty by

forfeiture of earnest money or can void the contract if the contract purchase price or cost exceeds the

reasonable value of the property established by the Department of Veterans Affairs.

The Escape Clause must be contained in the sales contract for all VA-guaranteed loans. Your lender is

responsible for ensuring that the paragraph is in the sales contract prior to closing. If the clause is not in

the sales contract, VA may not guaranty the loan.

VA Escape Clause:

"It is expressly agreed that, notwithstanding any other provisions of this contract, the purchaser

shall not incur any penalty by forfeiture of earnest money or otherwise be obligated to complete

the purchase of the property described herein, if the contract purchase price or cost exceeds the

reasonable value of the property established by the Department of Veterans Affairs. The

purchaser shall, however, have the privilege and option of proceeding with the consummation of

this contract without regard to the amount of the reasonable value established by the

Department of Veterans Affairs (38 U.S.C. 501, 3703(c)(1))."

This clause states that you have the option not to purchase a home when the appraisal’s Notice of Value

(NOV) is below the sales contract price. If the property doesn’t appraise, you will need to bring cash to

closing for the difference between the appraised value and the sales price (if unable to renegotiate with

the seller). If you don’t have enough remaining entitlement, you can make a down payment on the part

of the loan that exceeds the amount you have in entitlement to support. If the appraised value is less

than the sales price (after Reconsideration of Value (ROV) and renegotiation), bringing cash to closing is

the only option. (see VA Appraisal section below)

Other contingencies to consider are an appraised value contingency and a satisfactory home inspection

contingency. Your real estate agent can advise you if these or other contingencies are typical in your

real estate market.

VA Appraisal

Once you and the seller sign a purchase agreement, your lender (not you) will request a VA-approved

appraiser to provide an opinion of value of the home. All VA purchase and cash-out refinance loans

require an appraisal, which you must pay at this time.

The appraisal provides an appraiser’s opinion of value of the home and whether it meets VA’s minimum

property requirements. It also assures you and your lender that the value of the property is based on

facts and market data, not just the seller’s opinion. It can help give you confidence that the home you

want to purchase is worth the investment you are making.

24

Note: An appraisal is not a home inspection. You should consider hiring a qualified home

inspector to thoroughly inspect the home for defects and potential maintenance issues. (see

Home Inspections section below)

More information on the difference between a VA appraisal and a home inspection can be

found by viewing this short video. For more information on VA's minimum property

requirements, please watch this video.

When the appraisal is complete you will receive a notice of value (NOV). The NOV documents the

estimated value of the home, a list of comparable sales in the area, floor layout, photographs, and a list

of items requiring repair to meet VA minimum property requirements.

Your lender will request the appraisal in a timely manner after you submit your loan application. Lenders

should request the appraisal early in the loan process to avoid any potential process delays.

Note: Appraisers on the VA fee panel are NOT employees of VA, your lender, or your real estate

agent. They are licensed professionals with at least 5 years of experience to competently

appraise and value within your area.

What if my appraisal is below the purchase price?

If the appraised value is not enough to complete the loan, you have several options to enable you to

continue with the purchase:

• Request a Reconsideration of Value (ROV) – If you feel that the appraised value is less than it

should be, ask your lender or real estate agent to provide valid sales data to your lender to support

your opinion. VA staff will review the appraisal report the additional data that was provided, and

market data available in the VA Appraisal Management Service. (see Reconsideration of Value

section in Chapter 10 of the Lenders Handbook)

• Renegotiate the sale price – The seller may be willing to consider a reduced sale price that is equal

to or lesser than the appraised value. The seller can also offer other concessions for the sale. (see

Seller Concessions section in Chapter 8 of the Lenders Handbook)

• Bring cash to the closing table. If the ROV does not yield a higher value and the seller is unwilling to

negotiate a reduced sale price, you may have the option to pay the difference in cash at closing.

• Utilize your ‘Escape Clause’ – As stated above the ‘VA escape clause’ in your sale contract states

that you can opt not to purchase a home when the NOV is below the sales contract price. You can

get your earnest money back, but not any out-of-pocket home inspection or appraisal costs,

however it may be in your interest not to buy a home that is not worth the cost of buying or

repairing the home. Note: on new construction, you may pay for upgrades in advance, but if you do

not continue with the purchase, the upgrades are often not refundable or covered by the escape

clause.

• Request a “cost-approach” appraisal on new construction. This applies to new construction, if you

are building a home or you’re buying in a newly development area where there are no comparable

properties to estimate your home’s value. Your lender can request that the appraiser use a cost

approach to estimate value, as well as the sales approach.

25

For more information on appraisal cost and timeliness in your state, go to:

http://www.benefits.va.gov/HOMELOANS/appraiser_fee_schedule.asp.

For more information on the local VA appraisal requirements (such as wood-destroying insect

information) in your area, go to: https://www.benefits.va.gov/HOMELOANS/appraiser_cv_local_req.asp.

Home Inspections

Home inspections are not required by VA; however, a home inspection is highly recommended for every

borrower. We recommend that you choose an inspector that can give you an impartial assessment of

the home’s condition. The inspector should not have a conflict of interest in the sale. It is more

important that you get the value for your investment, and not just enter into another loan.

A home inspection is a process where a home inspector (licensed by the state) observes and provides a

written report of the systems and components of a property including but not limited to:

• Heating System

• Cooling System

• Plumbing System

• Electrical System

• Structural Components - foundation, roof masonry structure, exterior and interior components

or any other related residential building component recommended by the Home Inspection

Council and implemented by the Department through the regulatory process.

Note: Please note that it may be in your best interest to hire a structural engineer for your

inspection, especially for an older property. This type of inspection may cost more up front, but the

professional insight of an engineer can help you know if the home is structurally sound or requires

repairs or upgrades. You do not want to discover your home has major structural issues only after

buying the home.

Tips on picking a home inspector:

• Look for someone licensed to conduct inspections in your area

• Talk to your friends, family, and colleagues

• Search the web for inspectors and their reviews, if available

• Find someone not tied to any party in the sale of the home

What if my inspector finds a major issue?

Finding problems during an inspection is not a deal-breaker. In fact, an inspection gives you more

insight into the condition of the home that aren’t apparent to untrained eyes. Are the appliances

beyond their life expectancy and need replacing? What is the condition of the roof and foundation?

Knowing the issues can help you in re-negotiating with the seller. Perhaps they can lower their

asking price, make needed repairs/replacements, or make other concessions that may keep you

interested in the home. (*see Seller concessions in Chapter 8 of the Lenders Handbook)

As stated in the VA ‘Escape Clause’ section above, you may want to consider a satisfactory home

inspection contingency in your sales contract. Your real estate agent can advise you if these or other

contingencies are typical in your real estate market.

26

27

Negotiable items

You can negotiate the sale of the home up until the actual mortgage closing. Does the home price

exceed the VA appraisals reasonable home value? Does the home require repairs or upgrades?

Whatever the reason, as a buyer you can negotiate with your seller to find a middle ground that both

parties can agree.

Closing date of your loan

Earnest money

Funding Fee payment

Any party can pay for your funding fee (if you are not already exempt). This includes the seller and

your lender. Your family could also pay with gift funds.

Seller’s Concessions

VA allows sellers to pay closing costs, discount points, and any such concessions can be up to 4% of

the loan amount. (*See Seller Concessions section in Chapter 8 of the Lenders Handbook)

28

At Closing: Buying Your Home

Once you are ready to close on your home loan you will have to sign your documents and bring the

required money to the table. Your lender is required by law to provide you a Closing Disclosure at least

three business days before closing.

Note on Closing Disclosure: More information on the closing disclosure is available here. To see

an explanation for each part of the Closing Disclosure, go to:

https://www.consumerfinance.gov/owning-a-home/closing-disclosure/.

Closings may occur at a title company, escrow office, or attorney’s office depending on your area’s laws

or customary practices. You can expect to sign numerous documents including the mortgage, the note,

and the deed. During closing, expect your real estate agent to be present; an escrow officer or closing

agent to conduct the transaction; and the seller or a representative may or may not be at closing with

you.

This can be a lengthy process but always feel free to stop to ask questions if you have any. For more

information on what to expect at closing, please visit this link.

Fees and charges that you can pay

You can pay a maximum of:

• reasonable and customary amounts for any or all of the “Itemized Fees and Charges” designated

by VA, plus

• a one percent flat charge by the lender, plus

• reasonable discount points.

(*See Section 2 “Fees and Charges the Veteran-Borrower Can Pay” in Chapter 8 of the Lenders

Handbook)

Note on down payments: Remember, the VA-guaranteed home loan features a no down payment

option, unless required by your lender or if the purchase price is above the reasonable value of the

property, as determined by a VA appraiser. With no down payment, you can use those savings to further

grow your emergency fund or use the money on household expenses.

Once you are done with closing, the home is yours.

Congratulations!

29

Post-Purchase: Mortgage Servicing

The mortgage servicer is the company that handles the day-to-day tasks for managing your loan.

Typically, this includes processing loan payments, responding to your inquiries, keeping track of principal

and interest paid, managing the escrow account (if applicable), and sending you your mortgage

statements. A servicer may or may not be the same company that originated your loan.

You can identify your servicer by checking your monthly mortgage statement or payment coupon book.

If you cannot find a statement or coupon, you can try the Mortgage Electronic Registration System

(MERS®) Servicer Identification System toll-free at (888) 679-6377 or visit the MERS® website.

Borrowers can search for their servicer information on the MERS® website using

one of the following:

• MERS® System Mortgage Identification Number (MIN)

• Property Address Only

• Borrower Name and Property Address

• Borrower Name, SSN and Property Zip Code

• VA Case Number

*MERS is a private company that maintains information about mortgage loans and servicers.

VA encourages borrowers to contact their servicer to resolve any concerns they have with their existing

mortgage. Each servicer determines the best approach to fit individual borrower circumstances and are

required to comply with all applicable local, State, and Federal laws, such as the Real Estate Settlement

Procedures Act (RESPA)

7

, and regulations governing the VA Home Loan Program.

You may also call 1-877-827-3702, to contact the nearest VA Regional Loan Center and speak with a VA

representative regarding your individual home loan situation for counseling and guidance. Even

Veterans without a VA home loan can call the VA Regional Loan Center for questions about their loan.

If you have any unresolved disputes with your servicer (e.g., not applying payments, double billing,

transferring loan without a 15-day notice, etc.) you can contact:

• VA at 877-827-3702, or

• Consumer Financial Protection Bureau (CFPB) at https://www.consumerfinance.gov/about-

us/contact-us/ or 1-855-411-2372

Do I pay the same company that closed my loan?

Not necessarily. Some companies lend to borrowers and service (collect payments on) loans. It’s also

common for lenders to sell mortgages or to pay another company to service their loans.

Escrow Accounts

Sometimes called an impound account, an escrow account is an account set up by a mortgage lender to

pay certain property-related expenses. The mortgage servicer manages the account and takes a portion

of the mortgage payment to pay for taxes and homeowners insurance.

7

RESPA: https://files.consumerfinance.gov/f/201503_cfpb_regulation-x-real-estate-settlement-procedures-act.pdf

30

Note: Although principal and interest (P&I) remain the same, property taxes and insurance

premiums can change from year to year. Escrow payments—and with it, your total monthly

payment – will change accordingly.

Things to keep in mind about your escrow account:

• Read your annual escrow statement. This tells you what you owe or are owed at the end of the

year.

• If you do not have an escrow account, you are still responsible to pay taxes and insurance.

• Failure to pay your state or local taxes may result in a tax lien on your home and you could face

foreclosure.

• If you have automatic payments for your escrow, be sure to understand how your servicer will

change monthly payments when escrow shortages and surpluses occur.

More information on escrow accounts is available at: https://www.consumerfinance.gov/ask-

cfpb/what-is-an-escrow-or-impound-account-en-140/.

31

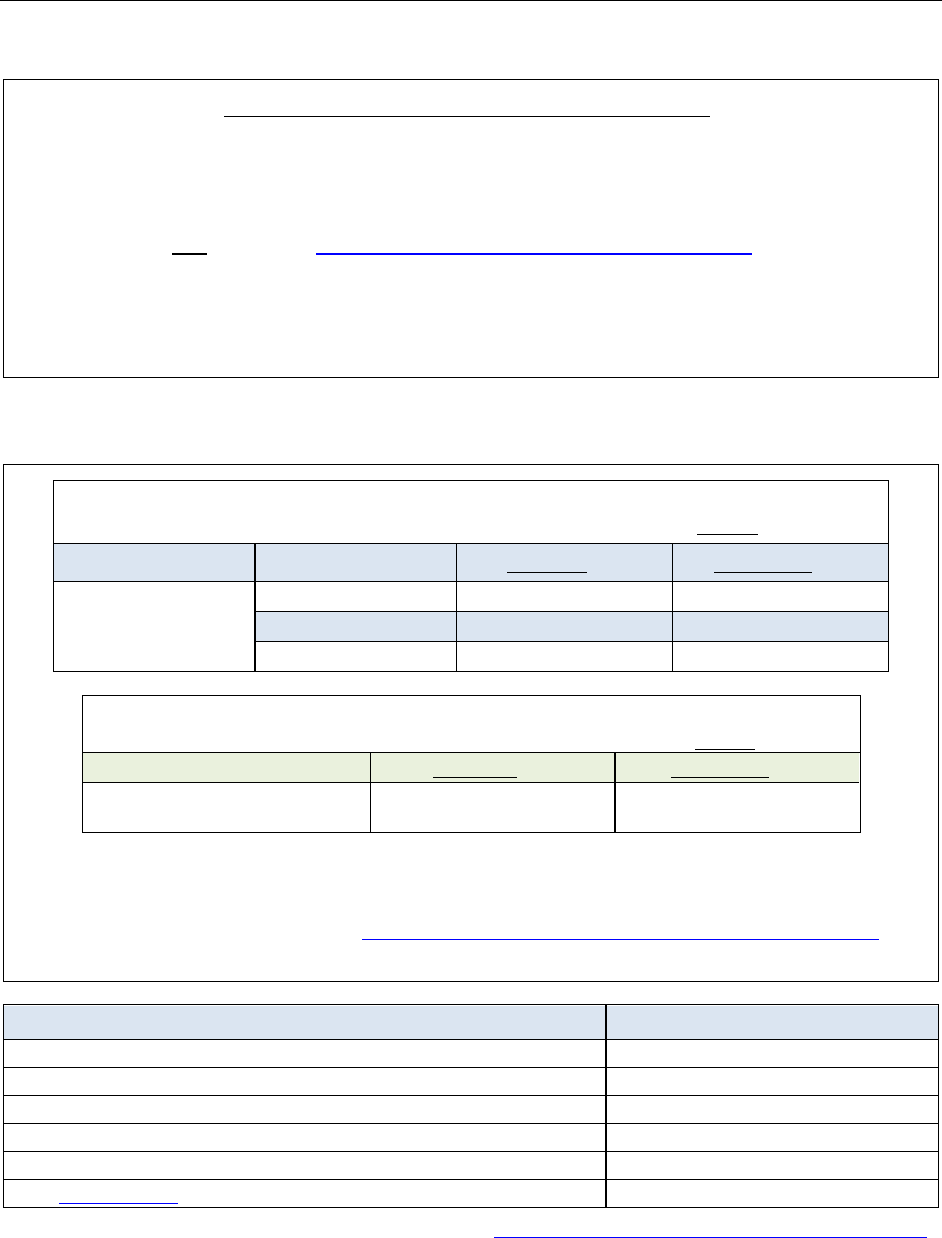

Appendix A: Military Service Requirements

Borrowers eligible a VA-guaranteed home loan must receive a military discharge that is NOT

dishonorable and meet the minimum service requirement based on era of service. More information on

eligibility is available in Chapter 2 of the VA Lender’s Handbook.

Veterans and Active Duty Service members

Date of service:

Minimum active-duty service

requirement:

Currently on active duty

90 continuous days

September 16, 1940 – July 25, 1947 (WWII)

90 total days

July 26, 1947 – June 26, 1950 (post-WWII)

181 continuous days

June 27, 1950 – January 31, 1955 (Korean War)

90 total days

February 1, 1955 – August 4, 1964 (post-Korean War)

90 total days

August 5, 1964 – May 7, 1975 (Vietnam War), OR

February 28, 1961 – May 7, 1975, if served in the Republic of

Vietnam

90 total days

May 8, 1975 – September 7, 1980 (post-Vietnam War), OR

May 8, 1975 – October 16, 1981, if served as an Officer

181 continuous days

September 8, 1980 – August 1, 1990, OR

October 17, 1981 – August 1, 1990, if served as an Officer

▪ 24 continuous months, OR

▪ The full period (at least 181 days)

if called to active duty

August 2, 1990 to present (Gulf War)

▪ 24 continuous months, OR

▪ The full period (at least 90 days) if

called or ordered to active duty

National Guard and Reserve members

Date of service:

Minimum service requirement:

August 2, 1990 to present

(Gulf War)

90 continuous days of active duty (i.e., ordered to active service under

Title 10 orders. Does NOT include active duty for training)

Any time period

6 creditable years

8

in the Selected Reserve or National Guard, AND at

least one of following must be true:

▪ Continue to serve in the Selected Reserve, or

▪ Discharged honorably, or

▪ Placed on the retired list, or

▪ Transferred to the Standby Reserve or an element of the Ready

Reserve other than the Selected Reserve after service

characterized as honorable

8

A credible year must include at least 16 points per anniversary year as seen on your retirement points statement.

(This can include 15 membership points plus Active Duty Training (ADT) and weekend drill points)

32

Exceptions to minimum service requirements

Service members discharged prior to meeting minimum service requirements may still be eligible for

a VA-guaranteed home loan if discharged for one of the reasons listed below:

• Hardship, or

• Convenience of the government (you must have served at least 20 months of a 2-year

enlistment), or

• Early out (you must have served 21 months of a 2-year enlistment), or

• Reduction in force, or

• Certain medical conditions, or

• A service-connected disability (a disability related to military service)

Other Than Honorable, Bad Conduct, or Dishonorable discharges

One of these discharge statuses may disqualify a Veteran from receiving VA benefits, including the VA

home loan benefit.

If the Department of Defense (DoD) or the Coast Guard determined you served honorably in one

period of service, you may use that honorable characterization to establish eligibility for VA benefits,

even if you later received a less than honorable discharge. You earned your benefits during the period

in which you served honorably. Make sure you specifically mention your period of honorable service

when applying for VA benefits.

You can apply for a discharge upgrade or correction, even if your previous upgrade application was

denied. For example, you may have additional evidence that wasn’t available to you when you last

applied, or the Department of Defense (DoD) may have issued new rules regarding discharges.

Note: DoD rules changed for discharges related to PTSD, TBI, and mental health in 2014,

military sexual harassment and assault in 2017, and sexual orientation in 2011.

You may want to consider finding someone to advocate on your behalf, depending on the complexity

of your case. A lawyer or Veterans Service Organization (VSO) can collect and submit supporting

documents for you. Find a VSO near you.